This is a rating that ranks the odds of a company surviving 12 months. The lowest score is 9 and the highest is 1. A score of 5 is good.

The credit limit recommendation shows what D&B has calculated to be a business’s borrowing capacity. It is a dollar amount recommendation for how much debt a company can handle. Creditors often use it to determine how much credit to extend.

This is an estimation of overall business risk on a scale of 4 to 1, with a score of 2 being considered good. The smaller the number, the better. It is a combination of letters and numbers. At the high end, a 5A rating indicates a company with a net worth of more than $50 million, while an HH rating at the low end represents a company with a net worth less than $5,000.

Here is how the composite part of this part of your D&B credit history works. First, it represents a company’s overall creditworthiness. It’s based on payment history, years in business, public records, number of employees and financial information. The scale ranges from 1 to 4.

It looks like this:

A score of one is the most creditworthy. If your company has not submitted financial information to Dun & Bradstreet, the highest they can get is a 2. This number is combined with the letter/ number combination above that indicates net worth. This gives an overall view of a company’s size and creditworthiness.

So, if a company has a rating of 4A3, the 4A part means the company’s net worth is $10,000,000 to $49,999,999, and the 3 indicates that the company is a “fair” credit risk.

If there isn’t enough data on a business to assign a regular Dun & Bradstreet credit rating, an alternative score known as a credit approval score is assigned. That one is based on the number of employees. Dun & Bradstreet will use any data they have available to calculate this alternative rating. A company can control this to a point by ensuring D&B has all of the information they need

Commercial credit score

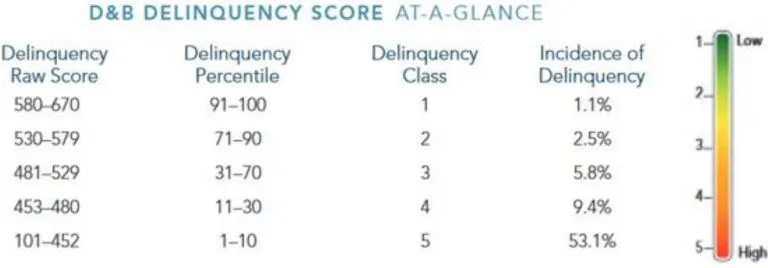

Measured on a scale of 101 to 670, the commercial credit score predicts the chance of a company becoming delinquent. A score of 101 means it is highly likely the company will be late with payments. A score of around 500 is often seen in a positive light.

Commercial Credit Percentile and Class

The scale runs from 0 to 100. It shows the chance of delinquency as well. But it measures this probability against other companies in the Dun & Bradstreet system. A score of 1 is the highest probability versus other businesses in the system. Most lenders consider a score of 80 or higher to be a good thing.

Payment History

This is your current payment status. It’s how many times accounts have become delinquent. It also shows how many accounts are currently delinquent, and overall trade balance.

Frequency

This one shows how many times your accounts have gone to collections. It also notes the number of liens and judgments you may have against you and your business. It also shows any bankruptcies related to your business or personal accounts.

Frequency also incorporates information about your payment patterns. Were you regularly slow or late with payment? Did you decrease the number of late payments over time? That affects your score.

Monetary

This specific factor focuses on how you make use of credit. For example, how much of your available credit are you using right now? Do you have a high ratio of late balances when compared with your credit limits?

Of course, if you are a new company owner, a lot of this information will not exist yet. Intelliscore handles this by using a blended model to identify your score. This means your personal credit score becomes part of determining your business's credit score.

Payment History

This is a one-page report that provides a summary of the business and its owner. Experian has found that a combined business-owner credit scoring model works better than a business or consumer only model. Blended scores have been found to outperform consumer or business credit scores alone by 10 – 20%.

This means that, with Experian, good business credit, in part, comes from a good credit score on the consumer side.

Experian Financial Stability Risk Score (FSR)

FSR predicts the potential of a business going bankrupt or not paying its debts. The score identifies the highest risk businesses by using payment and public records. They use many factors to make their predictions, including high use of credit lines, severely late payments, tax liens, judgments, collection accounts, high risk industries, and length of time in business.

How Long Does Data Stay on Your Experian Report?

According to Experian:

"Bankruptcies remain on file for 10 years after the filing date. Judgments for 7 years after the filing date. Tax liens for 7 years after the filing date. Collections remain on file for 6 years and 9 months after the last report date. UCC filings for 5 years after the last filing date. Bank, government and leasing data for 36 months. Trade data for 36 months after the last report date. Credit inquiries for 9 months."

How is the FICO SBSS Scored?

This score is vastly different from other business credit scoring models. The SBSS uses your business and personal credit scores. It also uses financial information like business assets and revenue. It aims to give a total global financial picture rolled into one score.

Business owners cannot access their FICO SBSS on their own. There is a proprietary formula for score calculations. FICO does not make that information public. You apply for a business loan blind about what your FICO SBSS credit score may be. This is unlike with the other credit agencies, where you can get a copy of your credit report and know where you stand.

The reason that the FICO SBSS does not work the same way is that you could have a different score for more than one business loan provider. This is due to how lenders ask for and get your FICO SBSS score.

The FICO SBSS Scoring Process

The process starts when you turn in your application. It will include all the financial documentation required by the financing provider. Then the business loan provider processes the information and sends it to FICO with a request for your SBSS score. At this point, they can ask for certain factors in the score to weigh more than others. For example, a business loan provier can put more weight on your personal credit score or your business credit. They could choose to weigh annual revenue as more important than payment history. It is their choice. As a result, your FICO SBSS score could vary between lenders.

First, FICO gets the request from the lender. FICO then searches business credit information from business CRAs. These include D&B, Experian, and Equifax. If they cannot pull enough scoring information from one, they move onto the next. If there is not enough data from any of them, then it uses personal credit and business financials only.

With the lender's weighting preferences, personal credit, business credit, and business financial data, they calculate the FICO SBSS. This information is specific to that lender.

Payment History

This is a one-page report that provides a summary of the business and its owner. Experian has found that a combined business-owner credit scoring model works better than a business or consumer only model. Blended scores have been found to outperform consumer or business credit scores alone by 10 – 20%.

Experian Financial Stability Risk Score (FSR)

FSR predicts the potential of a business going bankrupt or not paying its debts. The score identifies the highest risk businesses by using payment and public records. They use many factors to make their predictions, including high use of credit lines, severely late payments, tax liens, judgments, collection accounts, high risk industries, and length of time in business.

How Long Does Data Stay on Your Experian Report?

According to Experian:

"Bankruptcies remain on file for 10 years after the filing date. Judgments for 7 years after the filing date. Tax liens for 7 years after the filing date. Collections remain on file for 6 years and 9 months after the last report date. UCC filings for 5 years after the last filing date. Bank, government and leasing data for 36 months. Trade data for 36 months after the last report date. Credit inquiries for 9 months."

Update Your Record With the Credit Reporting Agencies

Update the information if there are errors or the relevant information is incomplete. At D&B, here’s where you can do so. For Experian, you can make corrections here. Find out what Equifax says about updating company information.

Business Credit Monitoring with Credit Suite

We can help you monitor business credit at Experian and D&B for considerably less than it would cost you at the CRAs. See: www.creditsuite.com/monitoring.

Disputes

Errors in your credit report(s) can be fixed. But the CRAs normally want you to dispute in a particular way.